Why Buy Cyber Liability Insurance? Because You Can’t Sweep a Breach Under the Rug

On October 23, 2019, New York’s “Stop Hacks and Improve Electronic Data Security Act (SHIELD) officially took effect. SHIELD is designed to protect New Yorkers’ private data and strengthen the state’s policies on data breaches.

All New York businesses must comply with SHIELD, which substantially expands the definition of “private information,” that, if comprised, requires businesses to notify the exposed.

This means that should a New York business experience a data breach that compromises Social Security numbers, driver’s license numbers, credit or debit card numbers, financial account numbers, biometric information, email addresses, and corresponding passwords, and security questions and answers, notification processes must take place.

In the U.S., notification costs can push $600,000. In 2018, hackers stole half a billion personal records and there’s no sign of them slowing down. When you put all the data together, we find that:

- Hackers want personal information

- They obtain personal information through data breaches

- Data breaches must be reported to affected parties

- Notification processes are expensive

What we haven’t even taken into consideration yet are the costs of potential litigation, information recovery, and computer system repairs. There’s also public fallout and damage to brand and reputation. Put simply, data breaches are business killers.

However, cyber liability insurance can help alleviate the pressure and damages caused by cyber-attacks and data breaches. Learn how as we explore cyber liability insurance on a deeper level and find out the answer to “Why buy cyber liability insurance?”

What is cyber liability insurance?

Cyber liability insurance protects businesses from the fallouts of cybercrime and data breaches. Cyber insurance covers:

- Notification fees

- Legal fees and expenses

- Restoring of personal identities of affected customers

- Recovering leaked and compromised data

- Repairing damaged equipment and computer systems

But like all insurance policies, cyber liability insurance has coverage limits. A policy will not cover:

- Potential future lost revenue

- Loss of value resulting from the theft of intellectual property

- Costs accrued improving internal technology systems, including software and security upgrades

Wait, doesn’t my general liability coverage handle these situations?

No, and that’s a common misconception amongst small business owners. Your general liability coverage will not handle any perils related to cybercrime. General liability coverage assists with third-party claims regarding bodily harm or damage to physical property, which would not include virtual files or personal information.

Okay, I get it. But my business isn’t at risk for cyber issues so why buy cyber liability insurance?

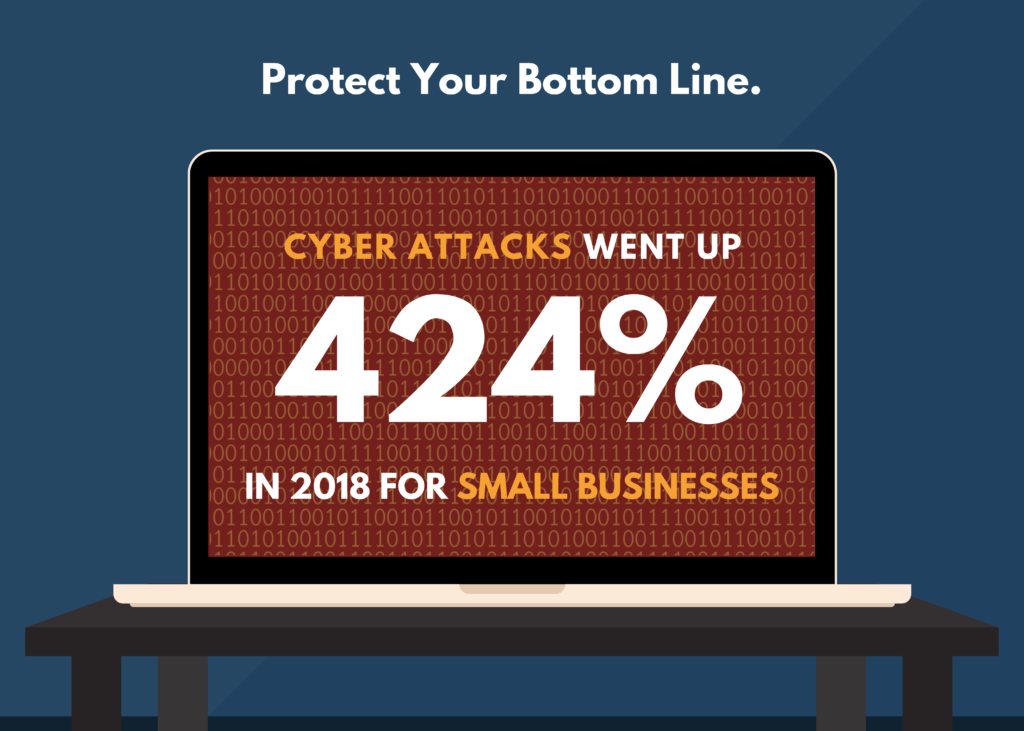

Another common misconception amongst small business owners. In fact, cyber-attacks were up 424% in 2018 for small businesses. But don’t take our word for it. Here are a few other reasons to take to heart when considering cyber liability insurance.

You have limited resources

Even if you have the technological skills to help your clients in the event of a data breach, the financial implications can cripple you. Notification costs alone are sky-high and the lawsuits can keep coming for years. Recovering from a cyber attack is not a one-person job. It requires the experience and manpower of multiple organizations, including an insurance company.

Your profits can be put on hold

When you’re dealing with a cyberattack, business isn’t likely to go on as usual. So while you’re dealing with notifications and other headaches, you’re not bringing in revenue. Cyber insurance offers coverage for lost profits in this exact situation.

It’s not all about breaches

Cyber insurance can help in other ways. Let’s say your social media team tries to take a sassy approach and ends up posting a defamatory comment about a competitor. Should your competition take legal action, cyber liability insurance can help cover legal costs.

Your reputation is everything

Maybe your company experiences a minor data breach. Notification costs are minimal, and no real damage comes to light. But your reputation can’t say the same. Leads stop coming in. Sales come to a halt. No one trusts your brand anymore. If you have cyber liability insurance, your policy may provide coverage for a public relations firm to step in and work their magic on your brand and audience.

As a business owner, you certainly have a lot on your plate. Don’t let the costs associated with a data breach get piled on top. Cyber liability insurance protects your business, your clients, and your future bottom line — because, without cybercrime coverage, your business’ longevity could be cut short.